In an increasingly fragmented world, investors are moving beyond traditional regional assumptions, evaluating nations individually through the lens of institutional strength, geopolitical stability, energy security and their ability to adapt to economic disruption.

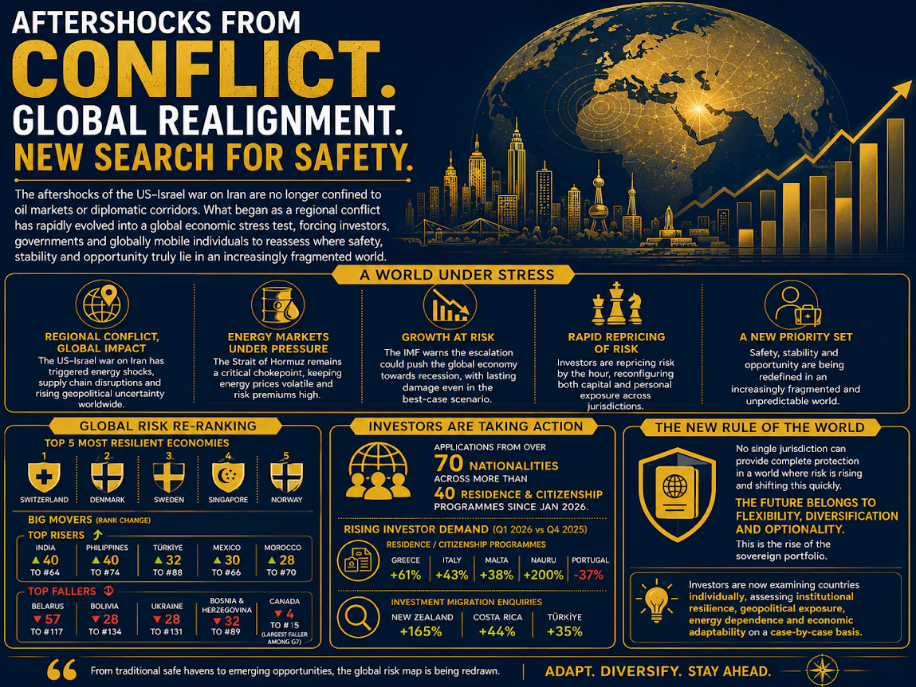

The geopolitical aftershocks of the US–Israel war on Iran are no longer confined to oil markets or diplomatic corridors. What began as a regional conflict has rapidly evolved into a global economic stress test, forcing investors, governments and globally mobile individuals to reassess where safety, stability and opportunity truly lie in an increasingly fragmented world.

The latest edition of the Henley & Partners–AlphaGeo Global Investment Risk and Resilience Index captures this shift with unusual clarity. Released against the backdrop of heightened geopolitical volatility and mounting fears of a global slowdown, the index reflects how markets are now repricing risk in real time, creating one of the sharpest re-rankings of countries seen in recent years.

The report arrives at a time when the International Monetary Fund has warned that the escalation in the Middle East could drag the global economy closer to recession, with even the most optimistic outcomes likely to leave long-term economic scars. Against this uncertain backdrop, investors are no longer relying solely on traditional assumptions of stability. Instead, they are actively reconfiguring both capital and personal exposure across jurisdictions.

Risk Repricing

At the heart of the analysis lies a striking observation — resilience and risk are no longer moving in tandem. Structural resilience, built over decades through strong institutions, stable governance and economic discipline, remains relatively steady. Risk perception, however, is now shifting by the hour.

Dr. Parag Khanna, Founder and CEO of AlphaGeo, described the current environment as a period of rapid and uneven global reordering, where markets are stress-testing countries against unfolding geopolitical realities rather than long-term reputations.

Traditional safe havens continue to dominate the top of the rankings. Switzerland retained the top position, followed closely by Denmark, Sweden, Singapore and Norway. The enduring dominance of Nordic economies reflects long-standing institutional credibility, fiscal prudence and investor trust rather than any sudden policy breakthrough.

Yet beneath this surface stability, a deeper transformation is underway. Markets are increasingly rewarding countries perceived as politically agile, strategically insulated and economically adaptable. Emerging economies that once sat on the margins of investor confidence are now gaining relative ground as global capital searches for resilience outside conventional centres of power.

Emerging Economies Including India Gain Investor Confidence

One of the most significant aspects of the latest rankings is the rise of several emerging economies. India emerged as one of the biggest gainers, climbing 40 places to rank 64th globally. The Philippines recorded an identical jump, while Türkiye, Mexico and Morocco also witnessed substantial improvements. These gains do not necessarily indicate that underlying fundamentals have transformed overnight. Rather, they reflect a broader reallocation of investor confidence. Countries with credible policy frameworks, expanding trade connectivity and the ability to absorb external shocks are increasingly being viewed more favourably than before, the report said.

The changing perception also signals the erosion of a long-standing global assumption — that developed economies are automatically safer while emerging markets remain inherently risky. Investors are now examining countries individually, assessing institutional resilience, geopolitical exposure, energy dependence and economic adaptability on a case-by-case basis.

China’s rise by six places to rank 31 further illustrates this trend. While geopolitical tensions surrounding China remain significant, improving market sentiment and investor expectations around economic management appear to have strengthened confidence in the country’s relative resilience.

Diverging Economies

The report also highlights how even established economies are no longer insulated from market scepticism. Canada emerged as the largest falling country among G7 nations, slipping four places to rank 15, reflecting concerns around fiscal pressures and political uncertainty.

Meanwhile, the United States and the United Kingdom remained unchanged, suggesting that investors continue to view them as structurally strong despite rising debt levels, political polarisation and exposure to global shocks.

Across Europe, the picture is increasingly complex. Core economies such as Germany and Italy registered modest improvements, while broader concerns around energy vulnerability, weak economic growth and political fragmentation continue to weigh on the continent’s outlook.

According to geopolitical commentators cited in the report, Europe’s resilience stems partly from its gradual political cohesion in response to external pressures. However, this same interconnectedness also amplifies vulnerability, particularly as shocks spread rapidly through energy systems, financial markets and investor sentiment.

Conflict Pressure

The Iran conflict has emerged as a defining catalyst in this evolving landscape. Beyond military implications, the war has intensified anxieties surrounding global energy security, trade routes and long-term geopolitical stability.

The Strait of Hormuz, one of the world’s most critical energy chokepoints, once again sits at the centre of investor concerns. Analysts believe that even if a negotiated outcome eventually emerges, the geopolitical risk premium attached to the region is unlikely to disappear anytime soon.

This uncertainty is already reshaping investor behaviour. Applications and enquiries for investment migration programmes have surged across several jurisdictions as globally mobile individuals seek greater optionality and security. Residence and citizenship programmes in Greece, Italy, Malta and Nauru have recorded sharp increases in demand, while enquiries linked to New Zealand, Costa Rica and Türkiye have also risen significantly.

Interestingly, demand patterns are becoming more selective rather than universally expansionary. Portugal, traditionally a favourite destination for investment migration, saw a notable decline in applications, indicating that investors are actively repositioning rather than simply increasing geographic diversification indiscriminately.

Strategic Mobility

What is emerging is a new philosophy of wealth preservation and personal security — one centred around sovereign diversification. Increasingly, investors are no longer treating citizenship or residency as lifestyle decisions alone. Instead, they are becoming strategic instruments for hedging geopolitical and economic risk.

Henley & Partners’ internal data reveals applications from more than 70 nationalities across over 40 residence and citizenship programmes since the start of 2026, underscoring how rapidly this shift is unfolding.

In the Gulf region, enquiries from UAE-based clients have risen sharply, driven largely by expatriate communities seeking additional mobility and long-term security options amid regional uncertainty. At the same time, interest in UAE golden visas has softened slightly, suggesting that investors are diversifying away from concentration risk rather than abandoning the region entirely.

The trend reflects a broader realisation that no single jurisdiction can offer complete protection in a world characterised by continuous geopolitical disruption and rapid repricing of risk.

New Reality

The current moment represents more than a temporary market reaction. It signals a structural transition towards a world where uncertainty is no longer episodic but persistent.

Investors are increasingly recognising that traditional assumptions about safe havens, developed markets and geopolitical stability are becoming less reliable. Instead, flexibility, diversification and optionality are emerging as the defining principles of modern global wealth management.

In this environment, the concept of a “sovereign portfolio” — spreading residency, citizenship, business interests and personal exposure across multiple jurisdictions — is gaining traction as both a financial and strategic necessity.

As geopolitical tensions continue to reshape trade flows, energy systems and global alliances, the latest Henley & Partners–AlphaGeo index suggests that the future of resilience will belong not necessarily to the richest or most powerful countries, but to those perceived as adaptable, credible and capable of navigating an increasingly unpredictable world order.