By Marshall Martin, Program Manager, and Nachiket Devasthale, Senior Consultant – Mobility Growth Advisory, Frost & Sullivan

India’s commercial vehicle (CV) industry is evolving as fleet operators increasingly prioritize utilization, fuel efficiency, uptime, and lifecycle economics over upfront acquisition cost.

LCV and MD/HD Truck Market Dynamics

Light commercial vehicles (LCVs) continue to be one of the fastest-growing segments in India’s commercial vehicle (CV) industry, supported by urban logistics, e-commerce, and last-mile delivery expansion. In contrast, medium- and heavy-duty (MD/HD) trucks remain closely tied to construction, industrial activity, and long-haul freight movement. Despite short-term macroeconomic uncertainties and cost pressures, the industry is expected to maintain stable momentum through FY2026–27, supported by investments in highways, freight corridors, logistics infrastructure, and urban development.

LCVs Remain a Key Growth Engine

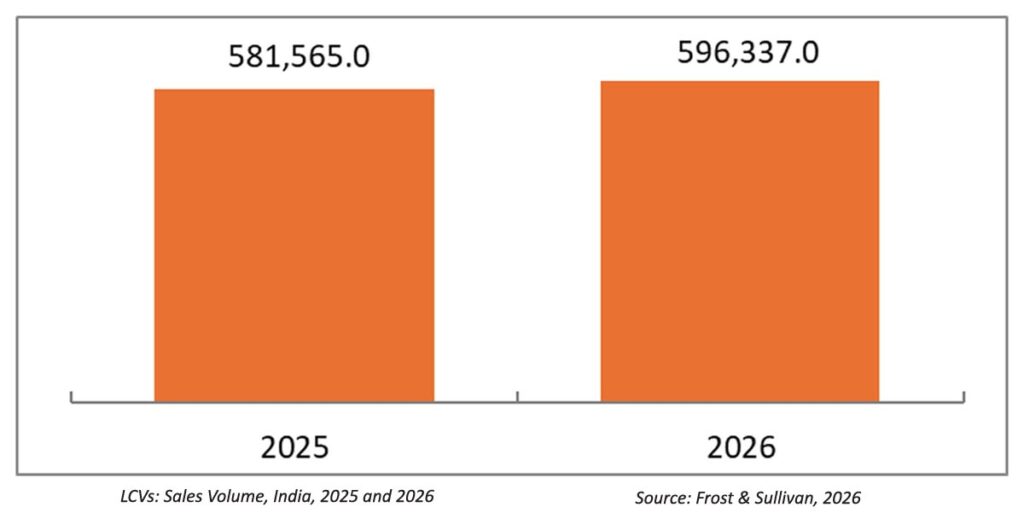

According to Frost & Sullivan analysis, LCV sales are projected to rise from nearly 582,000 units in 2025 to about 596,000 units in 2026, growing at a CAGR of 2.5%. The rapid expansion of quick-commerce platforms and same-day delivery services across metros and Tier-2 cities is increasing demand for small and mid-sized CVs. Simultaneously, adoption of higher-payload models is growing due to the focus on enhanced trip productivity and utilization.

Alternative powertrains are also gaining traction. By 2026, natural gas and Battery Electric Vehicles (BEVs) are expected to account for more than one-fifth of total LCV sales. While diesel will remain dominant, fleet operators are becoming more receptive to cleaner technologies, particularly in fixed-route urban applications with accessible charging/refueling infrastructure.

Leading manufacturers such as Tata Motors, Mahindra, and Ashok Leyland are expanding their CNG and electric portfolios. EV adoption, especially among e-commerce and intra-city logistics fleets, is being driven more by lower operating costs and predictable duty cycles than by sustainability goals alone.

Infrastructure and Freight Demand Support MD/HD Truck Growth

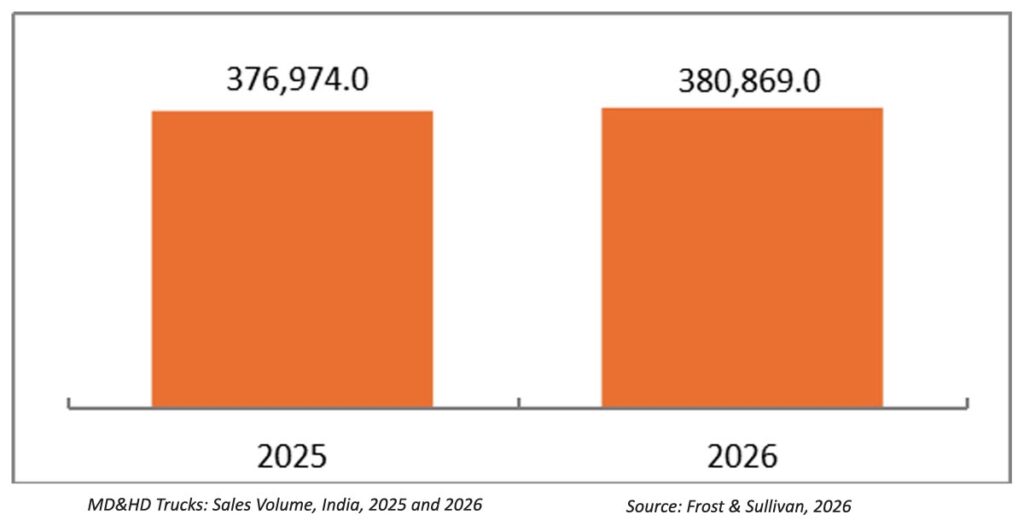

Demand in the MD/HD truck segment is expected to remain moderate but stable through FY2026–27, as per Frost & Sullivan analysis, sales are projected to reach nearly 381,000 units in 2026, growing by about 1% over 2025. Although growth will trail the LCV segment, replacement demand and infrastructure spending are expected to provide a stable base for the market.

Frost & Sullivan analysis indicates diesel is expected to account for more than 90% of MD/HD truck volumes over the next two years. However, natural gas emerges as a viable alternative in select long-haul applications. Meanwhile, manufacturers such as Tata Motors and Ashok Leyland are piloting battery electric and hydrogen fuel-cell solutions for specific applications, although long-haul electrification still faces challenges related to payload limitations and inadequate charging infrastructure.

Fleet Economics and Technology Reshape Purchase Decisions

One of the biggest shifts in India’s CV industry is the growing focus on lifecycle economics rather than just upfront acquisition costs. Fleet operators are increasingly evaluating vehicles based on fuel efficiency, uptime, maintenance support, and operating costs.

Consequently, telematics and remote fleet monitoring are becoming increasingly important, especially among organized fleets. Safety is also emerging as a key purchasing criterion, with manufacturers introducing technologies such as anti-lock braking systems (ABS) and driver monitoring solutions. Frost & Sullivan analysis indicates that upcoming stricter safety and emissions regulations, including ADAS-related requirements from April 2026, are expected to raise development costs and vehicle prices. While these changes may temporarily accelerate replacement demand, they could also slow fleet expansion if prices rise sharply.

India’s Bus Market in Transition

India’s bus market is undergoing a major transition driven by electrification, premiumization, digitalization, and rising passenger expectations. Traditionally a price-sensitive and volume-driven segment, it is evolving into a more organized and technology-enabled mobility ecosystem across urban, intercity, and long-haul operations.

At the core of this transformation is the reality that buses will remain India’s most scalable and affordable mode of mass transport. Passengers today increasingly expect cleaner interiors, digital ticketing, live tracking, greater comfort, and improved safety, compelling both state transport undertakings (STUs) and private operators to upgrade services.

Over the last five fiscal years, the market has also shifted toward lighter and higher-utilization segments. Mini and light buses have emerged as the largest volume drivers, supported by demand for school transport, staff mobility, and last-mile shuttle services. Meanwhile, traditional intercity coaches have gradually lost share as operators prioritize lower total cost of ownership (TCO)fleet categories and passengers shift toward air and rail travel. Premium AC and luxury coaches now account for nearly one-third of the market.

City Buses Are Undergoing Rapid Electrification

Electric buses have become the strongest growth driver in the segment. Government-backed programs like PM e-Bus Sewa and CESL aggregation initiatives are accelerating adoption through Gross Cost Contract (GCC) models that reduce the upfront burden on STUs.

Public operators such as BEST in Mumbai, BMTC in Bengaluru, and TGSRTC in Hyderabad have significantly expanded electric bus deployment, improving passenger perception through quieter cabins, smoother rides, and better service quality. Electric buses are increasingly being viewed as mainstream fleet replacement solutions rather than symbolic sustainability projects.

Premiumization and Branded Mobility Ecosystems Gain Ground

STUs are also becoming more premiumized. Operators such as MSRTC and KSRTC are expanding premium services, including Shivneri, Shivshahi, Airavat, and Ambari buses, while also exploring business-travel and airport connectivity solutions.

In parallel, private intercity operators such as IntrCity, SmartBus, and Zingbus are building branded mobility ecosystems centered on digital ticketing, centralized fleet monitoring, comfort, and punctuality. Premium AC sleeper coaches are among the fastest-growing categories on routes such as Mumbai–Goa, and Bengaluru–Hyderabad. NueGo’s electric intercity operations also demonstrate the growing viability of electric coaches beyond urban applications.

Advanced Technologies and Alternative Fuels Gain Momentum

Diesel continues to dominate long-haul and interstate operations due to range and charging limitations. However, premium coach manufacturers are introducing advanced telematics and enhanced passenger comfort features. LNG and hydrogen pilot projects are also beginning to emerge in select sustainability-focused corridors.

Despite this progress, challenges persist. STUs remain financially stressed due to aging fleets and regulated fares, while private operators confront rising diesel prices and driver shortages. The EV ecosystem also faces hurdles such as delayed GCC payments and inadequate charging infrastructure outside major metros.

Meanwhile, updated AIS-119 sleeper bus safety standards backed by stricter enforcement are expected to push operators toward safer factory-built buses instead of customized aftermarket body structures.

The Road Ahead

By FY2026–27, India’s CV industry is expected to become more efficient, connected, and technology-driven. LCVs will continue benefiting from urban logistics and e-commerce growth, while MD/HD truck demand will remain tied to infrastructure and freight activity. Alternative fuels, especially natural gas and EVs, will steadily gain traction. Simultaneously, India’s bus market will become increasingly premiumized, electrified, digitally integrated, and safety-focused, with reliability, comfort, and operational efficiency becoming as important as affordability.