Daimler Truck Holding AG delivered resilient Group financial performance for FY2025, operating within its guided range despite a challenging macroeconomic environment marked by declining key markets and tariff headwinds.

The company reported market-leading results in North America despite weak demand conditions, while Mercedes-Benz Trucks delivered solid profitability. Daimler Buses achieved double-digit margins for the first time, supported by a strong fourth-quarter performance, and Trucks Asia recorded robust results driven by positive developments in Indonesia and the Middle East. Financial Services also improved its return on equity through sustained cost discipline.

For the full year, Daimler Truck posted an adjusted Group EBIT of €3,778 million compared to €4,667 million in 2024. Revenue from the Industrial Business declined to €45.9 billion from €50.7 billion in the previous year, while the adjusted return on sales stood at 7.8%, down from 8.9%. Free Cash Flow from the Industrial Business came in at €1,824 million compared to €3,152 million in 2024, although the fourth quarter delivered a strong cash generation of €1,747 million. Earnings per share stood at €2.56 versus €3.64 in the prior year. The company has proposed a stable dividend of €1.90 per share, unchanged year-on-year.

Leadership Signals Confidence Amid Headwinds

Karin Rådström, President and CEO of Daimler Truck, noted that the company delivered improved operational performance despite a demanding business environment. She highlighted that Daimler Truck maintained market leadership in North America and Europe in the medium- and heavy-duty truck segments, achieved double-digit profitability in its bus business, and recorded significant order intake in defence. She added that the company is executing its efficiency measures ahead of plan and remains committed to driving industry transformation at a pace aligned with customer needs.

Eva Scherer, CFO of Daimler Truck, emphasised that the company maintained a strong financial foundation, delivering a 7.8% return on sales and net industrial liquidity of €7.7 billion. She stated that Daimler Truck is positioned for operational improvement in 2026, supported by higher volumes and efficiency gains that are expected to offset increased tariff effects. With rising order momentum, she expects the second half of the year to be stronger than the first. She also highlighted that, including the expected cash inflow from the Fuso–Hino integration, the company anticipates a significant increase in Free Cash Flow in 2026 while continuing to deliver consistent shareholder returns.

Operational Performance Reflects Resilience

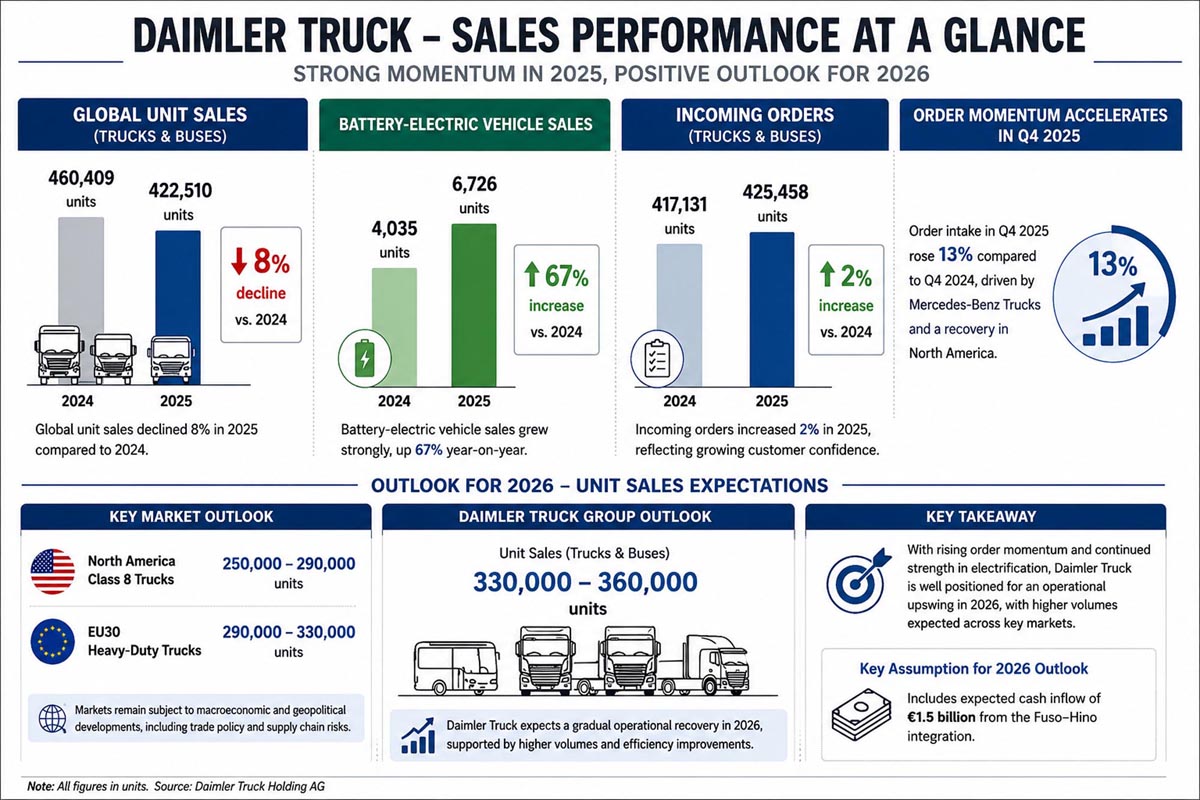

In operational terms, Daimler Truck sold 422,510 trucks and buses globally in 2025, representing an 8% decline compared to 460,409 units in 2024. However, the company recorded strong growth in its electrification journey, with battery-electric vehicle sales increasing by 67% to 6,726 units from 4,035 units in the previous year. While revenue declined by 10% and adjusted EBIT fell by 19%, the company demonstrated resilience through improved order intake, which rose by 2% to 425,458 units. Notably, order momentum accelerated in the fourth quarter, with a 13% increase driven by Mercedes-Benz Trucks and a recovery in North America.

Looking ahead to 2026, Daimler Truck expects a gradual operational recovery supported by higher volumes and efficiency improvements, although tariff pressures are likely to persist. The company forecasts the North American Class 8 truck market to range between 250,000 and 290,000 units, while the EU30 heavy-duty truck market is expected to range between 290,000 and 330,000 units. Unit sales are projected to be between 330,000 and 360,000 units. Revenue from the Industrial Business is expected to be in the range of €42 billion to €46 billion, with adjusted EBIT forecast between €3.2 billion and €3.7 billion. The adjusted return on sales is expected to range between 6% and 8%, while Free Cash Flow is anticipated to reach between €2.7 billion and €3.2 billion, including an expected €1.5 billion cash inflow from the Fuso–Hino integration. The outlook remains subject to macroeconomic and geopolitical uncertainties, particularly developments in US trade policy and potential supply chain disruptions.

Strategy Anchored in Technology and Market Expansion

From a strategic standpoint, Daimler Truck continued to strengthen its position as a global leader in the commercial vehicle industry through advancements in product innovation, technology, and operational efficiency. In Europe, the company accelerated its transition to zero-emission mobility, with strong performance from products such as the Mercedes-Benz eCitaro city bus and the eActros 600 long-haul truck. It also achieved a leading 35% market share in battery-electric trucks in the EU30 region. At the same time, Daimler Truck continued to enhance its diesel portfolio to meet diverse customer requirements.

In India, the company expanded its heavy-duty portfolio with new BharatBenz truck models for the construction and mining segments, leveraging domestic volumes to support future export growth. In Latin America, the introduction of the all-new Mercedes-Benz Axor further strengthened its product offering, particularly in higher tonnage applications.

In North America, Daimler Truck commenced series production of the Fifth Generation Freightliner Cascadia, reinforcing its leadership in the Class 8 segment. Its bus business further strengthened its market position through a manufacturing partnership with Otokar, enabling cost-efficient production to meet growing demand for the Mercedes-Benz Conecto city bus.

The company also made notable progress in its defence business, securing major contracts including an order for 7,000 Mercedes-Benz Zetros trucks for the French Army. Defence revenues are now expected to reach €1 billion by 2028, ahead of the original 2030 target.