By Ravichandran Srinivasan

Step into any modern car showroom, and you are greeted by an orchestrated symphony of luxury: high-ceilinged glass atriums, the intoxicating scent of premium leather, and a fleet of shiny new models reflecting the glow of recessed LEDs. To the casual observer, it looks like a gold mine. But behind this polished facade, the automotive retail sector is navigating a severe profitability crisis. The traditional franchise model, which served the industry for a century, is currently being crushed between rising operational costs, shifting consumer habits, and rigid manufacturer demands.

Here is a deep dive into the systemic failures keeping dealerships in financial gridlock and the radical shifts required to shift back into gear.

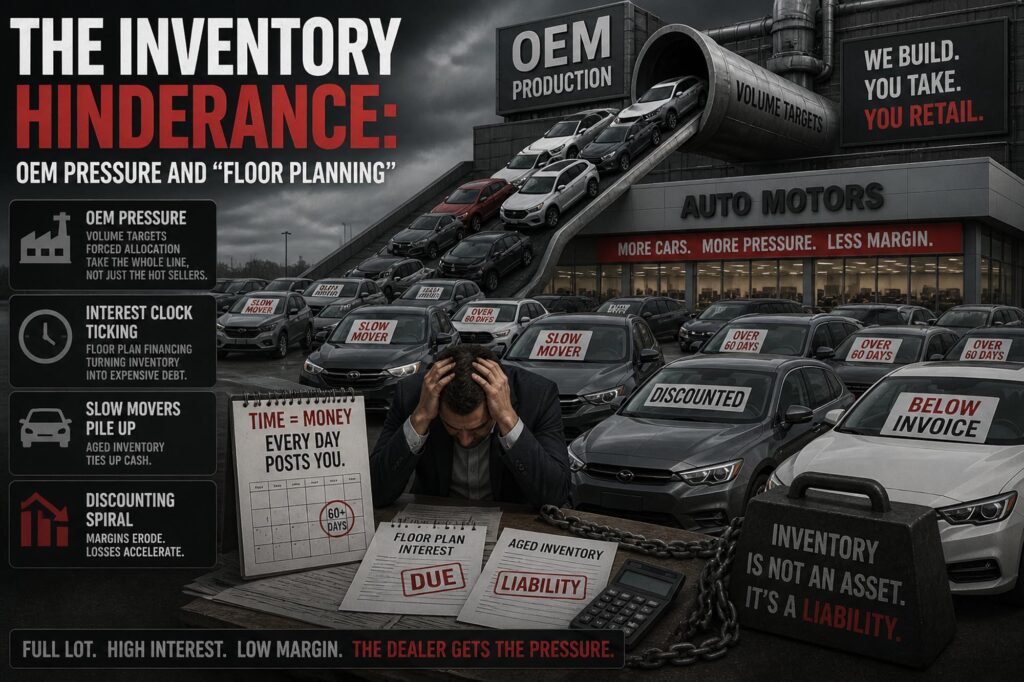

The Inventory Hinderance: OEM Pressure and ‘Floor Planning’

The fundamental friction in the automotive world exists between the Original Equipment Manufacturer (OEM) and the dealer. OEMs operate on volume; their success is measured by “wholesales”—the number of cars they push out of the factory gates to the dealers. Consequently, dealers are often treated as a shock absorber for factory overproduction.

- The Interest Trap: Most dealers do not own their inventory outright; they rely on Floor Plan Financing. In an era of fluctuating interest rates, the cost of carrying 100 or 200 cars on a lot is astronomical. When a vehicle sits for more than 60 days, it transitions from an asset to a liability.

- The “Slow-Mover” Problem: To get the high-demand SUVs, OEMs often force dealers to accept a “balanced” portfolio—meaning for every bestseller, they might have to take three slow-moving sedans in unpopular colors.

- Erosion of Margin: When the lot is full and the bank starts calling for interest payments, dealers panic. This leads to forced discounting. To move metal, dealers slash prices, often selling vehicles at or below the “invoice price,” hoping to recoup the loss through manufacturer volume bonuses that may never materialize.

The Myth of Service Department Immunity

Historically, the “Fixed Operations” (service, parts, and body shop) was the dealership’s financial fortress. Industry experts look at the Absorption Ratio—the percentage of a dealership’s total overhead covered by service and parts profits. The gold standard is 100%, but the reality for many modern dealerships has slipped below 60%.

Several factors are dismantling the workshop’s profitability:

- Rising Tech Costs: Modern cars are computers on wheels. Keeping a workshop updated requires constant investment in proprietary diagnostic tools and high-voltage equipment for EVs, .

- The Talent Gap: There is a chronic shortage of master technicians. To retain talent, dealers must pay premium wages, yet they struggle to pass these costs onto customers who are increasingly price-sensitive and prone to visiting independent garages once their warranty expires.

- EV Reliability: The rise of Electric Vehicles poses a long-term threat. With roughly 20 moving parts in an electric drivetrain compared to 2,000+ in an internal combustion engine, the frequency of lucrative fluid changes and engine repairs is plummeting.

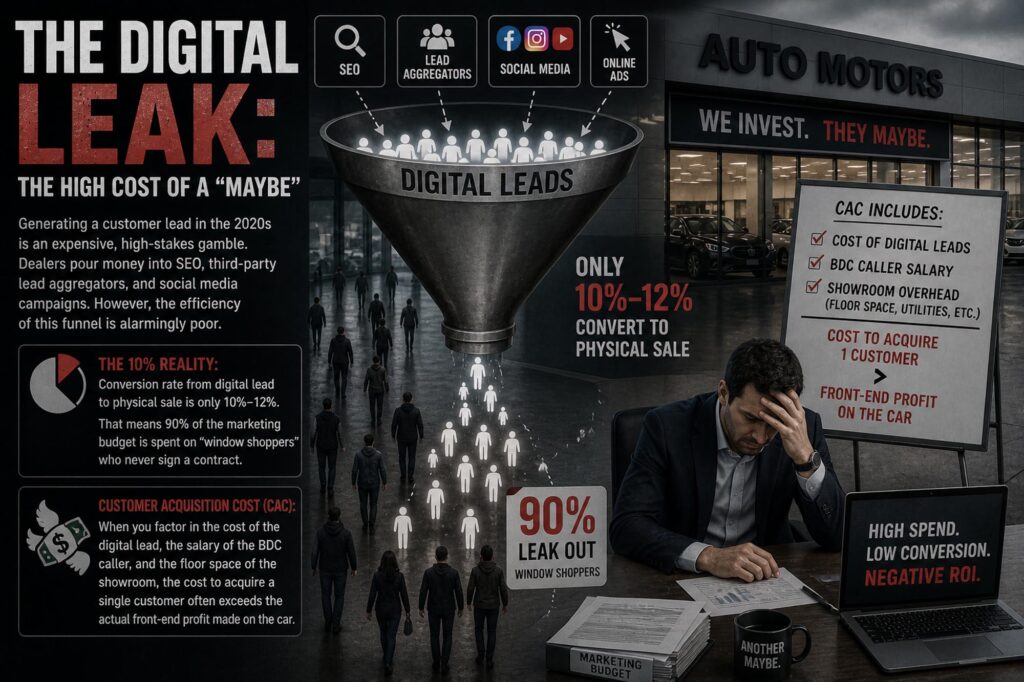

The Digital Leak: The High Cost of a “Maybe”

Generating a customer lead in the 2020s is an expensive, high-stakes gamble. Dealers pour money into Search Engine Optimization (SEO), third-party lead aggregators, and social media campaigns. However, the efficiency of this funnel is alarmingly poor.

- The 10% Reality: On average, the conversion rate from a digital lead to a physical sale hovers around 10% to 12%. This means that 90% of a dealer’s marketing budget is essentially spent on “window shoppers” who never sign a contract.

- Customer Acquisition Cost (CAC): When you factor in the cost of the digital lead, the salary of the Business Development Center (BDC) caller, and the floor space of the showroom, the cost to acquire a single customer often exceeds the actual front-end profit made on the car.

The ‘Price Shopper’ and Race to the Bottom

The internet has empowered the consumer but commoditized the dealer. A sales consultant might spend five hours with a family, conducting multiple test drives and explaining complex safety features, only for the customer to leave and call five other dealerships within a 100-mile radius.

If “Dealer B” offers the same car for INR 5-10000 less, the customer often jumps ship. This “Price Shopping” phenomenon creates a toxic environment where the dealership providing the best service is punished, while the dealership willing to take the biggest loss wins the sale. This race to the bottom demotivates top-tier sales talent and turns car buying into a cold, transactional experience rather than a relationship-based one.

The Shrinking Safety Net: F&I and VAS

When the “front-end” profit on a car sale is zero (or negative), dealers rely on Finance and Insurance (F&I) and Value-Added Services (VAS) like extended warranties and ceramic coatings. But this safety net is fraying.

- Cash is King (for the Customer): In the premium and luxury segments, particularly in markets like India, a significant portion of buyers are “cash rich.” Finance penetration in the (INR 20 lacs+) segment can be as low as 25%. When a customer pays cash, the dealer loses the commission they would have earned from a bank.

- Direct-to-Consumer Insurance: Many buyers now use aggregators to find their own insurance, bypassing the dealer’s marked-up policies.

- Transparency Pressures: Regulators are increasingly scrutinizing “add-ons,” making it harder for dealers to include high-margin items like nitrogen-filled tires or window etching without explicit (and often rejected) customer consent.

The Agency Model: A Glimmer of Hope?

To solve this, a radical shift is beginning to take hold, particularly in the luxury space (Mercedes-Benz, various EV startups). This is the Agency Model.

| Traditional Model | Agency Model |

| Dealer buys stock from OEM | OEM owns the stock |

| Dealer sets the final price | One price, set by OEM (No haggling) |

| High financial risk for dealer | Low financial risk; fixed commission |

| Focus on “Closing” | Focus on “Customer Experience” |

Under this system, the dealer acts as a facilitator. They provide the test drive and the delivery, and in return, they receive a guaranteed fee per car. This eliminates the “Price Shopper” dilemma and removes the crushing weight of inventory interest from the dealer’s balance sheet.

The Road Ahead

The automotive dealership is at a crossroads. The “Stuck in Neutral” phase cannot last forever; either the engine will stall, or the industry must shift gears. For dealerships to survive, the relationship with OEMs must move from a adversarial push-model to a collaborative pull-model.

Success in the next decade will not belong to the dealer who can shout the loudest about discounts, but to the one who can streamline their operations, embrace transparent pricing, and pivot their service centers to handle the high-tech, low-maintenance reality of the future. The gleam in the showroom must once again be matched by the strength of the balance sheet.