By Chris Fisher, Senior Commercial Vehicle Analyst, and Jim Downey, Vice President, Global Data Products, Power Systems Research

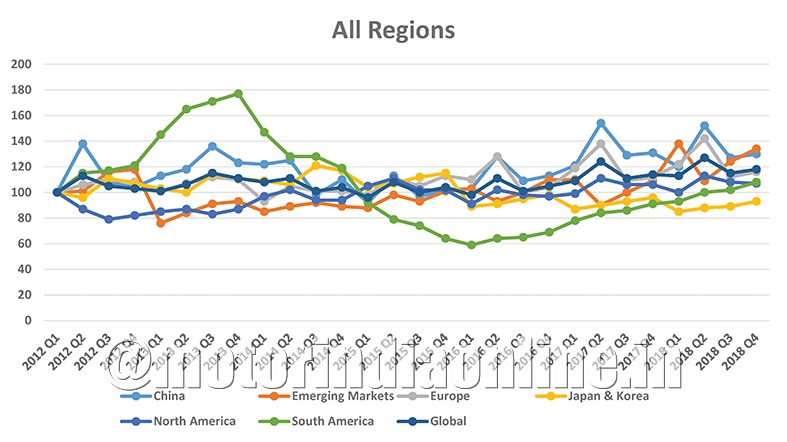

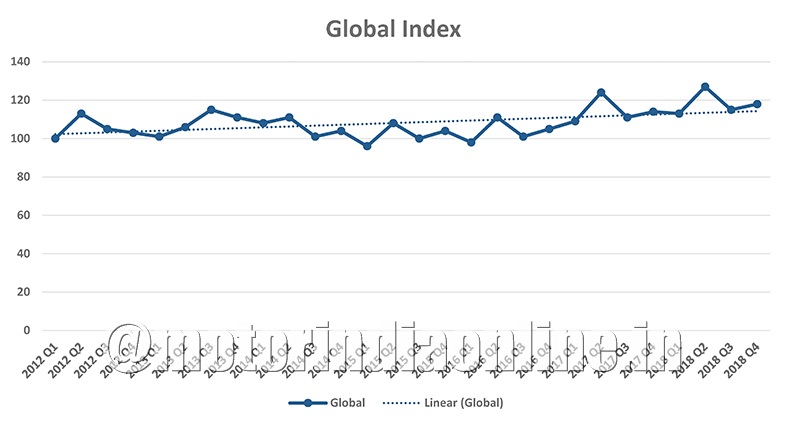

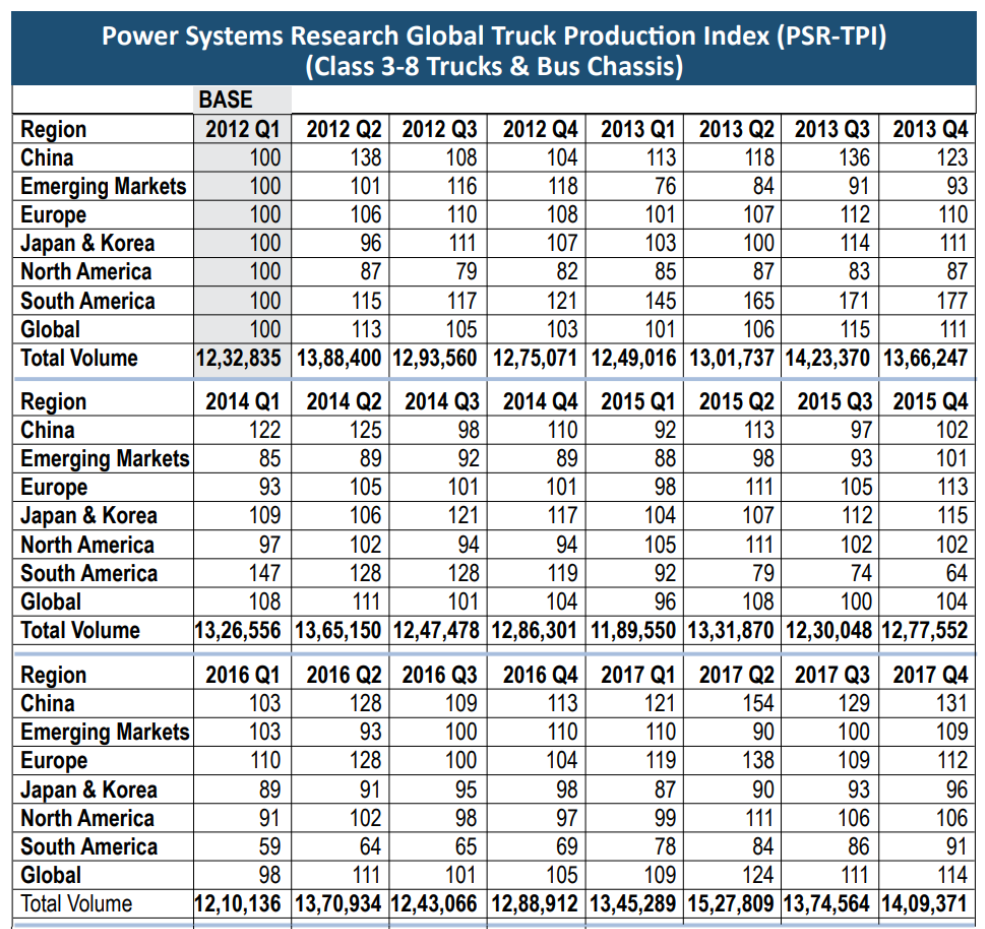

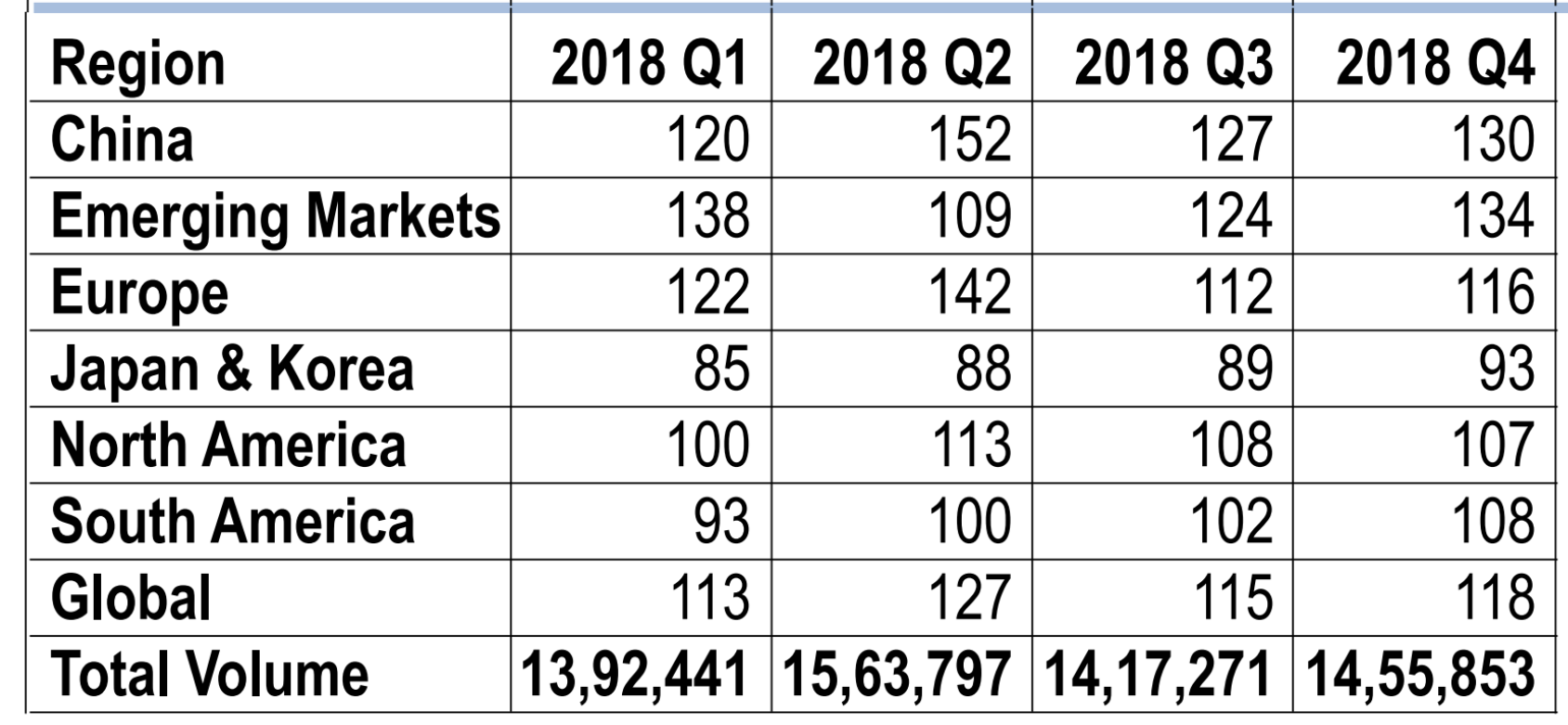

The Power Systems Research Truck Production Index (PSR-TPI) increased from 115 to 118, or 2.6%, for the three-month period ended December 31, 2018, from Q3 2018.

The year-over-year (Q4 2017 to Q4 2018) gain for PSR-TPI was 3.5%, climbing four points from 114 to 118.

The PSR-TPI measures truck production globally and across six regions – North America, China, Europe, South America, Japan & Korea and emerging markets.

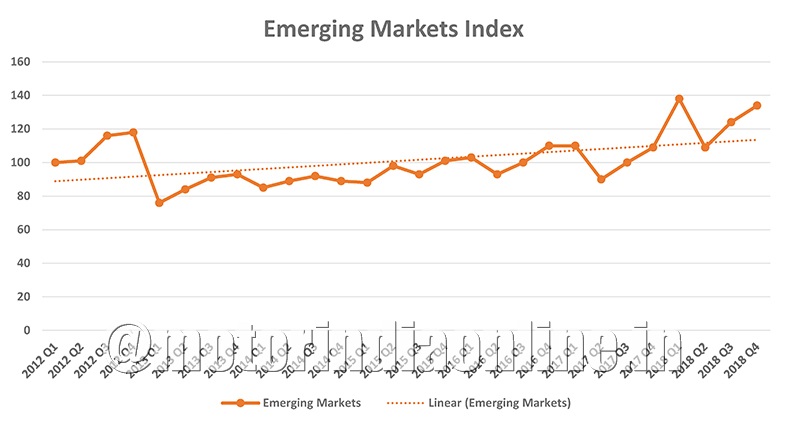

This data comes from CV Link™, the proprietary database maintained by Power Systems Research. Except for North America, most of the other key regions are beginning to see an economic slowdown.

Regarding the commercial truck market, a slowing global economy along with generally strong truck sales during the past few years is placing downward pressure on commercial vehicle adoption rates.

While the economic condition in the US is currently strong, the economy is expected to moderate later in 2019 and into 2020. The anticipated economic slowdown in the US is expected to contribute to a global economic slowdown over the next few years.

North America

The medium and heavy commercial truck segment is expected to remain strong through much of 2019. Production levels for class 8 trucks continue to be strong, driven by record order levels that are expected to continue well into 2019. Order boards are basically filled through the first half of the year.

The strong economy is driving the need to replace or expand fleets. While not as strong as the heavy truck segment, the medium truck segment is having another good year driven in part by strong consumer and vocational demand.

Europe

Medium and heavy truck production is expected to increase by 2.6% in Greater Europe this year over 2018. Heavy truck production may improve by 1.7% while medium truck production is expected to increase by 6.5% over 2018. After weak demand in Eastern Europe over the past few years a recovery in demand is in full swing. While demand in Western Europe has slowed somewhat, it continues to be historically strong.

South Asia

Following strong demand in 2018, medium and heavy truck production is projected to decline by .8% this year over 2018. In 2018, demand in India was very strong after lower demand in 2017, primarily due to the implementation of the BS-IV emission regulations which increased the cost of trucks. Additional infrastructure spending is sure to boost demand in India during the next few years.

South America

Commercial vehicle demand in Brazil is expected to continue the positive trend after a number of years with very low sales primarily due to poor economic conditions. Domestic and export sales started improving in 2017 and continued through last year. While truck exports are a main reason for this increase, domestic demand has also significantly improved during the past year. Demand in Argentina may soften as the country struggles with its economy.

Japan / Korea

After lower medium and heavy truck demand in 2018, production levels are expected to be flat this year. Production continues to be transferred from Japan and Korea closer to their traditional export markets.

Greater China

As a result of the GB1589 regulations to control overloading of trucks last year, commercial truck demand was very strong in 2017 and into the first eight months of 2018. However, a slowing economy and relatively high truck capacity and higher truck prices partly due to the cost of emission technology and lower freight rates, demand is expected to decline in the fourth quarter and somewhat stagnate throughout the forecast period.

The next update of the Power Systems Research TPI will be in April next and will reflect changes in TPI during the first quarter of 2019.