As governments prioritise food security and emerging economies ramp up investment in cold storage infrastructure, the cold chain industry is poised for a new era of growth.

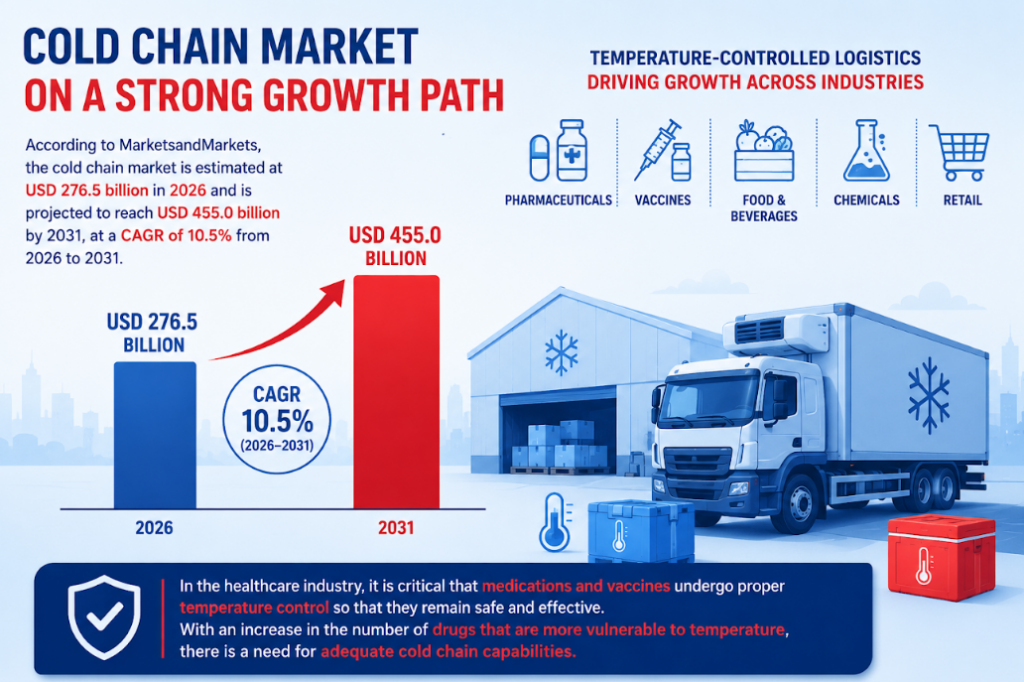

The global cold chain market is on a strong growth trajectory, valued at $276.5 billion in 2026 and projected to reach $455 billion by 2031, growing at a CAGR of 10.5%. Once considered a niche logistics segment, temperature-controlled supply chains have become a critical backbone across multiple industries — from food and pharmaceuticals to fine art and electronics.

What Is Driving the Growth?

According to the recent report by MarketsandMarkets, the surge in demand is being fuelled by several converging forces. The rise in temperature-sensitive medications and biologics has made cold chain capabilities indispensable in healthcare. Simultaneously, the boom in online grocery shopping and international food trade has pushed food and beverage companies to invest heavily in refrigerated logistics. Add to this the global expansion of pharmaceutical distribution and organised retail, and the result is a market seeing investment from all directions.

Food & Pharma Lead the Charge

Among all applications, food and beverages command the largest share of the cold chain market. Perishables such as dairy, meat, seafood, fruits, and vegetables depend entirely on temperature-controlled logistics to reach consumers safely. The pharmaceutical sector follows closely, where even minor temperature deviations can render vaccines and biologics ineffective — a risk no healthcare system can afford.

Refrigerated Transport

By type, refrigerated transport dominates the market, valued at nearly $105 billion in 2025 and expected to grow at a CAGR of 10.7%. Within this, Light Commercial Vehicles (LCVs) are emerging as the fastest-growing sub-segment, projected to register an 11.5% CAGR. Their agility in urban environments, lower operating costs, and alignment with sustainability goals make them the vehicle of choice for last-mile cold chain delivery.

Asia Pacific Leads, Europe Holds Firm

Asia Pacific is the undisputed regional leader, accounting for over 66% of global cold chain revenue in 2025 — driven by large populations, growing middle classes, and rapid expansion of organised retail and pharmaceutical sectors across China, India, and Southeast Asia.

Europe, meanwhile, remains a significant force, underpinned by stringent regulatory frameworks governing food safety and pharmaceutical transport. Countries such as Germany, France, the UK, and the Nordic countries continue to invest in advanced cold storage infrastructure, aided by robust logistics networks and widespread IoT adoption.

Technology as the Game Changer

Modern cold chain logistics is increasingly tech-driven. IoT-based temperature monitoring, automated refrigeration systems, and energy-efficient storage facilities are transforming how perishables are tracked and managed across supply chains. These innovations are not only improving efficiency but also ensuring compliance with tightening global regulations — making technology adoption less of a choice and more of a necessity.

The Road Ahead

With emerging economies stepping up investments in cold storage infrastructure and governments prioritising food security and post-harvest loss reduction, the cold chain market is set for sustained expansion. As global trade in temperature-sensitive goods continues to rise, cold chain logistics will only grow in strategic importance — making it one of the most compelling infrastructure plays of the decade.