Basic HTML Version

MOTORINDIA

l

March 2012

97

are thus forging alliances with glo-

bal peers in order to enhance their

product offerings. The global com-

ponent manufacturers are also keen

to get a foothold in the Indian auto

sector to overcome the stagnation in

their home countries.

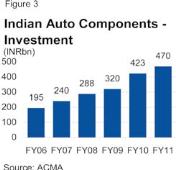

The capex plans of domestic auto

suppliers are significantly large in

relation to their own internal cash

generation. An important point to

note is that investments in this sec-

tor did not slow down in the past

even in the downturn years as most

OEMs and auto component suppli-

ers are taking a long-term view of

the Indian market.

Fitch notes that the funding mix

is critical in the current situation

where auto suppliers have to under-

take capex towards product expan-

sion to weather slower growth in

auto volumes. Many domestic auto

suppliers have raised funds from

private equity to support their ex-

pansion plans on top of the financial

assistance from the collaborators.

Though the trend of private equity

infusion will continue in 2012 on

account of the sector’s growth pros-

pects, the agency expects that bor-

rowings would also increase for the

majority of domestic auto suppliers

to fund their capex plans. However,

this would not likely affect the credit

metrics of the suppliers as they are

expected to be broadly in line with

their current ratings.

w

market outlook

Besides the collaborative

approach, many large do-

mestic suppliers are un-

dertaking such expansion

through the acquisition of

smaller suppliers in do-

mestic and global markets.