Basic HTML Version

96

MOTORINDIA

l

March 2012

cash conversion cycle along with

poor credit availability can severely

impair their ability to carry on with

capex plans, which is imperative to

help suppliers weather the impact

of slowing auto sales through en-

hanced product offerings.

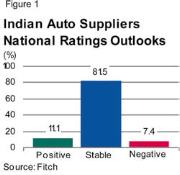

Key issues

The current macro-economic sce-

nario points toward slowing domes-

tic vehicle sales over the near term,

which could hamper the revenues

for auto suppliers. The 2008-09 eco-

nomic slowdown prompted these

companies to diversify their rev-

enue streams and segment exposure.

Though many auto suppliers started

targeting niche segments such as

off-road vehicles, farm equipments

and heavy machinery manufactures,

their contribution to the auto suppli-

ers’ revenue remains very low cur-

rently. As a result, auto suppliers

continue to rely on OEMs through

the supply of more components.

The developments over the last

year have also prompted a large

number of OEMs in India to step up

localisation of components which

are currently being imported. The

force majeure events in one area,

like the tsunami in Japan in early

2011 and the recent floods in Thai-

land have the potential for the dis-

ruption of the automotive supply

chain in some other area by affecting

the supply of critical components.

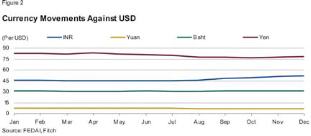

Besides, adverse currency move-

ments can affect the cash flows of

OEMs. A sudden and sharp depreci-

ation of the rupee has made imports

costlier and hurt OEM profitability,

more so in cases where such imports

are meant for domestic demand.

Fitch expects that increasing share

of local components in a vehicle

would keep the growth momentum

for domestic suppliers despite sub-

dued vehicle volumes.

Growing competition

International trade dynamics are

undergoing changes due to various

bilateral or regional trade agree-

ments, which call for closer co-oper-

ation between the

signatories. Such

agreements could

potentially affect

Indian auto sup-

pliers by increas-

ing competition

in international

geographies due to the higher duty

structure for them in comparison to

the preferred trade partners of im-

porting nations. As a result, Indian

auto suppliers could be compelled

to invest in increasing efficiencies

to counter the rising competition in

global markets.

The domestic auto component in-

dustry is likely to witness high com-

petition in the wake of such trade

agreements entered into by India

with its trading partners, particularly

in Asia. The domestic suppliers, so

far, are largely protected from im-

ports in the low value and low tech-

nology products due to higher duties

and other trade barriers, which these

pacts aim to eliminate over the me-

dium to long term.

The auto suppliers have to regu-

larly invest in improving operational

efficiencies, which are necessary to

remain competitive and to protect

operating margins. These are con-

stantly under pressure due to rising

input costs – all of

which cannot be

passed on to the

OEMs.

The

capacity

additions and ef-

ficiency improve-

ment initiatives

themselves require large invest-

ments for the auto suppliers, and

thus may limit their ability to pursue

opportunities for product expansion

which increasing localisation may

create. Many Indian auto suppliers

market outlook

Large-scale investments

by OEMs towards capacity

expansion and new model

launches entail invest-

ments for their auto sup-

pliers as well.