By Darshan Kudva, Executive Director – Automotive and Sudipta Das, Manager – Automotive, PwC

India’s commercial vehicle (CV) industry stands at the cusp of steady growth, propelled by a dynamic blend of market evolution, regulatory reforms, and rapid technological advancements. Forecasts suggest that this sector will expand at a compound annual growth rate (CAGR) of 4 to 6 percent through FY30, buoyed by India’s robust economic momentum – with GDP growth expected to reach 6.3 percent by FY26 – and sustained investments in core infrastructure sectors such as steel and cement.

Segmental Performance and Near-term Trends

The Indian CV space is diverse, encompassing Heavy Commercial Vehicles (HCV), Intermediate and Medium Commercial Vehicles (I&MCV), Light Commercial Vehicles (LCV), and Small Commercial Vehicles (SCV), along with a growing passenger vehicle segment focused on buses.

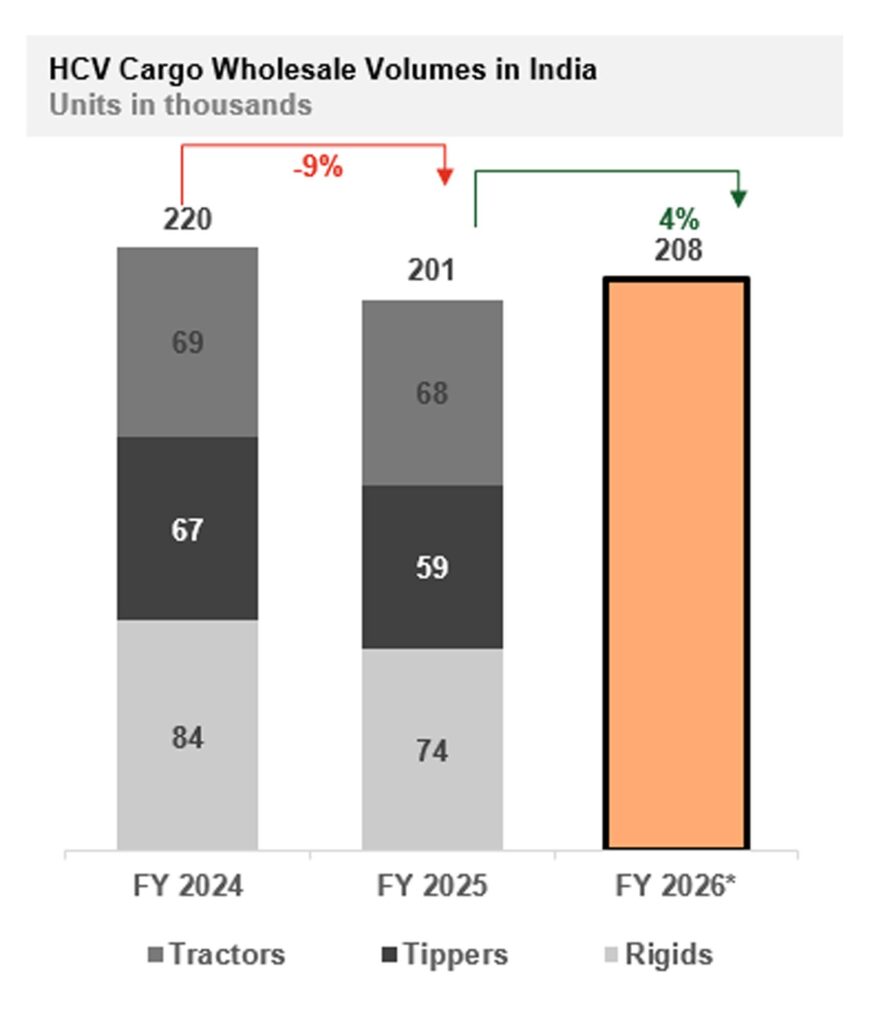

- Heavy Commercial Vehicles (HCV): After witnessing a volume dip of approximately 9 percent in FY25 due primarily to high inventory, stalled mining activity, and dealer stock adjustments, the outlook is optimistic. HCV sales are expected to rebound with a 4 percent growth forecast for FY26. This resurgence is supported by increasing freight demand – road freight is growing steadily at a 6 percent CAGR – alongside policies encouraging the scrappage of ageing vehicles. Additionally, investments in infrastructure such as the Golden Quadrilateral highway and major National Highways (with NHAI bidding ₹3.4 lakh crore in FY26) are fueling demand. Equally exciting is the push towards alternative powertrains, exemplified by the ambitious Green Hydrogen Hub initiative in Andhra Pradesh, with a projected investment of ₹1.85 lakh crore.

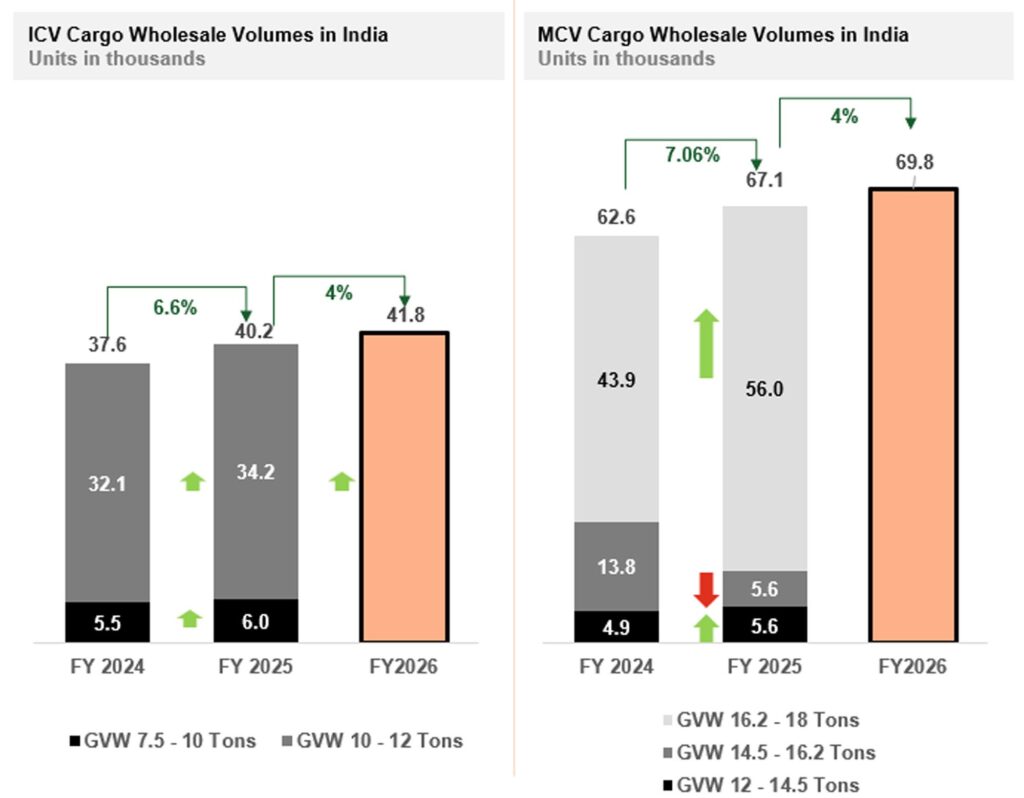

Intermediate & Medium Commercial Vehicles (I&MCV): This segment is expected to grow by 4 percent in FY26, particularly driven by 18.5-ton Medium Commercial Vehicles. Growth catalysts include the rise of e-commerce and fast-moving consumer goods (FMCG) sectors, which favor payload-efficient vehicles, as well as increasing rural transportation needs linked to agricultural development. The ongoing scrappage policy and replacement demand also provide a boost here.

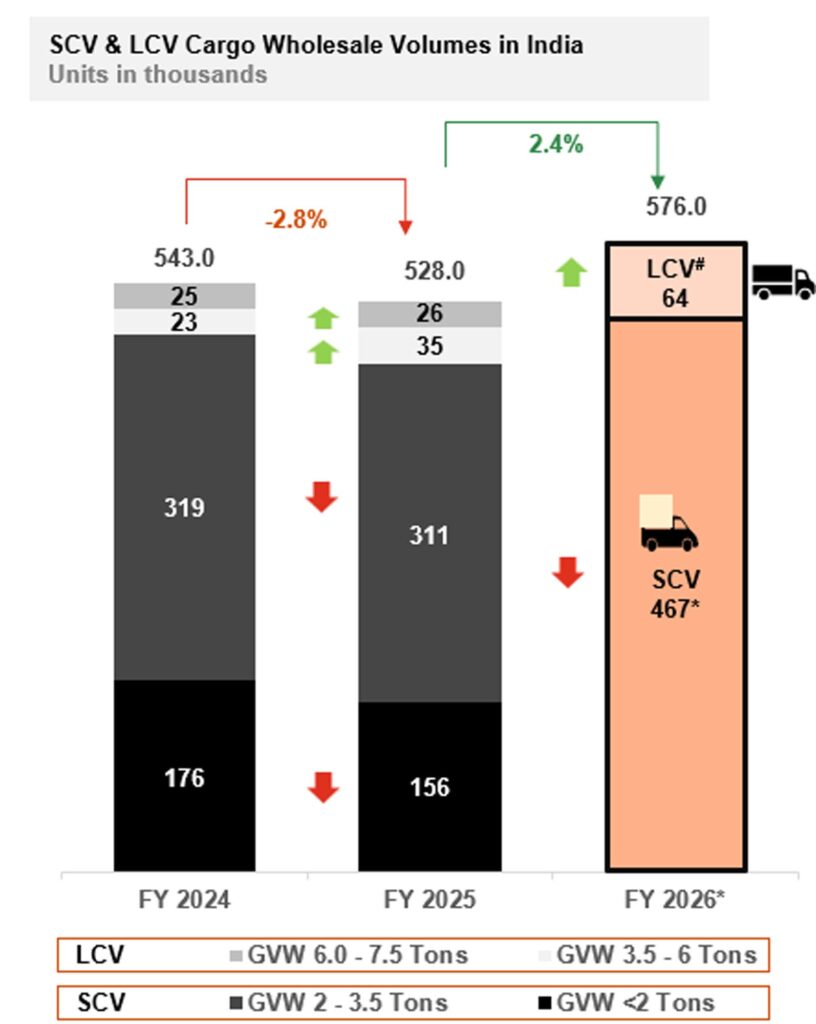

- Light Commercial Vehicles (LCV) and Small Commercial Vehicles (SCV): While SCVs are predicted to remain stagnant, LCVs are poised for moderate growth of about 4 percent in FY26. This growth is largely driven by expansion in e-commerce operations, especially across tier 2 and tier 3 cities. Moreover, electric three-wheelers are gaining traction in the ‘less than 2-ton GVW’ segment as environmentally friendly alternatives to internal combustion engine (ICE) vehicles, while also offering a lower total cost of ownership (TCO).

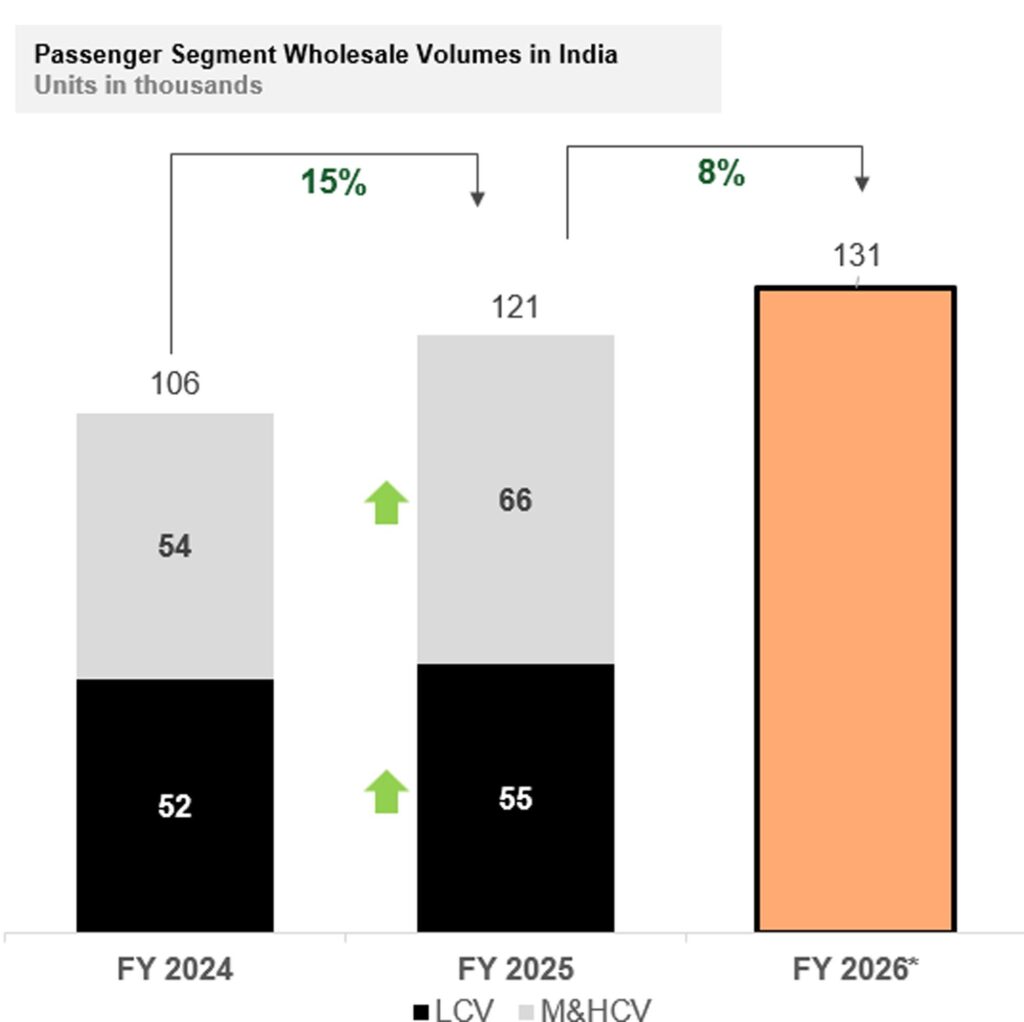

- Passenger Vehicles (Buses): The bus segment continues its upward trajectory, with sales projected to rise 8 percent in FY26, marking a third successive year of growth. Government initiatives, notably the PM E-Drive scheme, which has allocated nearly ₹44 billion for the purchase of 14,028 electric buses in FY26, are accelerating the shift to electric mobility. This shift is reinforced by environmental benefits, payment security improvements, policy revisions within State Transport Undertakings (STUs), and the Net Zero ambitions pushing out older fleets.

Driving Forces Behind Industry Evolution

Several overarching trends and forces are shaping the future of Indian CV market.

1. Dynamic Policy Environment

Regulatory frameworks are increasingly aligning the industry toward cleaner, safer, and more sustainable products. The introduction of Phase III Corporate Average Fuel Efficiency (CAFE) norms targeting fuel efficiency by 2027, and the anticipated adoption of Euro 7 emission standards, reflect this commitment. The Securities and Exchange Board of India (SEBI) is mandating greenhouse gas tracking as part of phased Business Responsibility & Sustainability Reporting (BRSR), reinforcing environmental accountability. In parallel, Extended Producer Responsibility (EPR) policies are incentivizing scrappage with a focus on recycling. New safety mandates are set to standardize advanced features such as Forward Collision Warning Systems (FCWS), Electronic Stability Control (ESC), Autonomous Emergency Braking Systems (AEBS), and cybersecurity protocols. Additionally, lawmakers are proposing limits on truck driver hours to 8 hours per day for safety, complemented by plans to develop over 1,000 rest stations nationwide.

2. Changing Customer Preferences

Indian commercial vehicle customers are pivoting towards modern solutions that prioritize efficiency, connectivity, and safety. Predictive maintenance is gaining widespread adoption, as demonstrated by Force Motors’ iPulse platform, which leverages AI to reduce breakdowns and optimize fuel consumption. The rapid expansion of e-commerce continues to reshape fleet requirements: it accounted for 7–10 percent of Tata Motors’ CV sales and 25 percent of Ashok Leyland’s in metro areas as of FY21. Simultaneously, leasing and direct-to-customer (D2C) models are growing rapidly; nearly half of commercial EV fleet operators now favor leasing options available through players like Mahindra Electric and financial service providers like Revfin. Digital platforms are also revolutionizing after-sales service, with OEMs investing in command centers capable of remote diagnostics and 24/7 support, enhancing ownership experiences.

3. Disruptive Technological Innovations

Innovation is no longer optional but essential. Manufacturers are embracing AI, cognitive technologies, telematics, and connected vehicle platforms to transform mobility. Ashok Leyland’s connected commercial vehicles generate over three million data points per hour, enabling real-time fleet insights. Tata Motors is piloting AI-driven fleet analytics while launching India’s first hydrogen internal combustion engine truck, signifying a path toward diversified powertrains. Startups like Taabi Mobility employ AI for route and idling optimization, helping fleets cut fuel costs substantially. The emergence of software-defined vehicles (SDVs) and real-time diagnostics promises further leaps in operational efficiency.

4. Road and Infrastructure Development

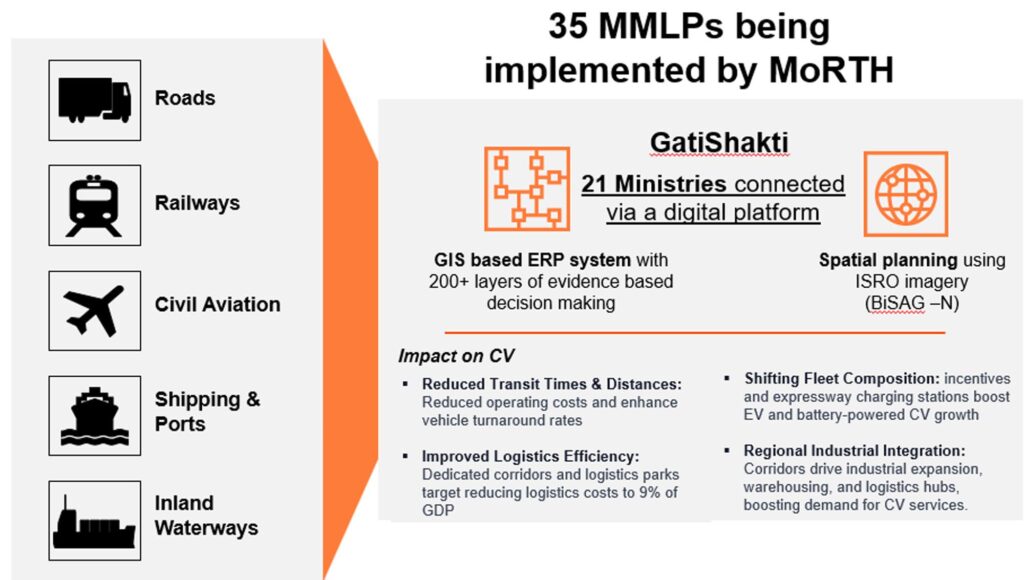

Government infrastructure programs are transforming logistics in India. Dedicated Freight Corridors (DFCs), Multi-Modal Logistics Parks (MMLPs), and the Gati Shakti initiative are all geared toward improving supply chain efficiency. These corridors aim to more than double rail freight capacity from 1,617 million tonnes to nearly 3,300 million tonnes by 2030, shifting modal freight dynamics substantially. These changes increase demand for last-mile delivery vehicles – LCVs, MCVs, and SCVs – while potentially moderating the growth of the HCV segment. The government’s strategic vision includes establishing 11 industrial corridors and 2 defense corridors, alongside creating clusters in pharma, medical, fishing, and harbor sectors, all of which will enhance cargo handling capabilities and associated commercial vehicle demand.

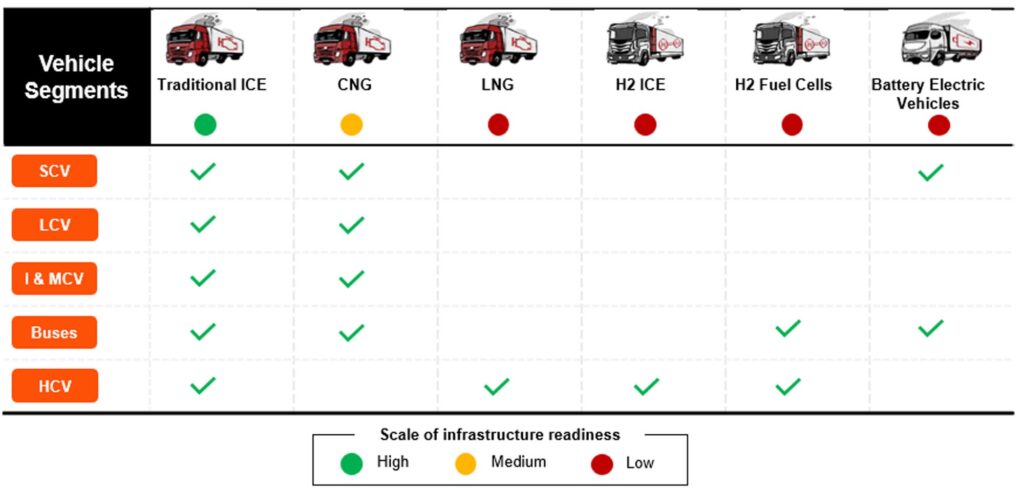

5. Emergence of Alternate Powertrains

The future will be powered by a mix of propulsion technologies tailored to use cases, contributing to better total cost of ownership (TCO) and customer satisfaction. Electric vehicles already lead in urban passenger transport and short-haul logistics, while hydrogen and hybrid models are gaining ground in long-haul and heavy-duty segments. This diversification ensures that manufacturers can meet evolving regulatory requirements and market preferences with an array of solutions.

In Conclusion

India’s commercial vehicle industry is entering a transformative decade. Backed by strong macroeconomic growth, proactive policies, evolving customer needs, and breakthrough technologies, the sector is poised for sustained expansion. Manufacturers who navigate the evolving regulatory environment, embrace innovation, and understand shifting customer expectations stand to lead the market forward. Meanwhile, infrastructure development and alternative powertrains will reshape the logistics landscape, unlocking opportunities across every commercial vehicle segment.

The road ahead for India’s commercial vehicle industry is promising – driven by progress, powered by innovation, and steered by sustainability.