By Kinjal Shah, Senior VP & Co-Group Head, Corporate Ratings, ICRA Limited

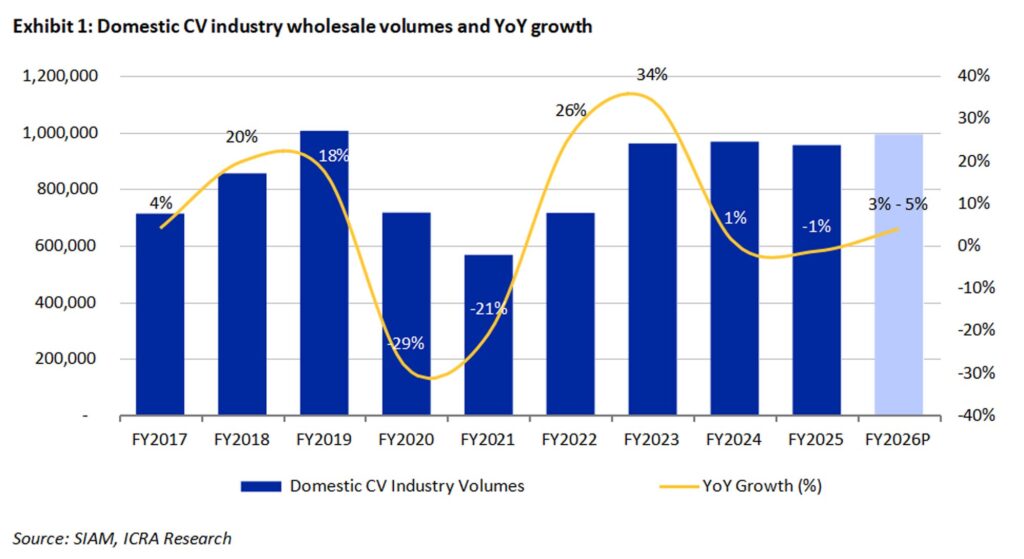

ICRA forecasts the domestic CV industry to report a modest 3-5% growth in wholesale volumes in FY2026, aided by improving pace of construction and infrastructure activities which had been muted in early FY2025 due to the General Elections. This follows two years of subdued performance of the industry, with 1% growth in FY2024 and 1% decline in FY2025.

Among the various sub-segments within the CV industry, the medium and heavy commercial vehicles (M&HCV) (trucks) volumes in FY2026 are forecasted to report a nominal growth of 0-3% YoY, supported by increased demand from construction and mining sectors, and consequently higher freight availability.

Domestic light commercial vehicles (LCV) (trucks) wholesale volumes are projected to grow by 3-5% YoY in FY2026 aided by a largely steady economic environment and ongoing recovery in the e-commerce segment.

The scrappage of older Government vehicles is expected to drive replacement demand for the bus segment from state road transport undertakings (SRTUs) in FY2026, supporting a growth of 8-10%.

Some key trends shaping the sector over the recent past:

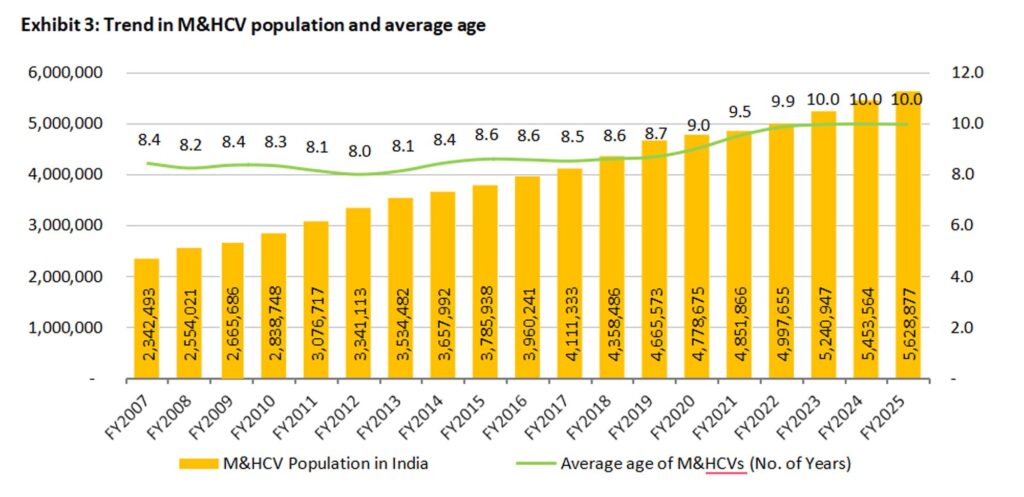

- Replacement demand on the rise with an ageing fleet: Ageing vehicular fleet and Government mandates are the two key drivers of replacement demand in India. As per ICRA’s estimates, the average age of M&HCVs increased to around 10 years in the FY2023-FY2025 period, the highest in the past two decades, resulting in operating inefficiencies for fleet operators. ICRA expects replacement demand to play a key role in spurring sales over the medium to long term. Superior operating economics and load-carrying capacity of new trucks, as well as comfort features, such as factory-fitted cabins, AC cabins, and higher horsepower offerings augur well for replacement demand. The Scrappage Policy, which came into effect from April 1, 2023, has not induced a volume surge so far; however, we expect the same to support replacement demand over the medium term, especially for the bus segment.

- Preference for heavier trucks: There has been a gradual shift towards higher tonnage trucks, with the tonnage growth outpacing volume growth for a major part of the last decade, with gross vehicle weight (GVW) in M&HCV trucks doubling over FY2010 to FY2024. This shift has been supported by multiple factors, including the superior economic viability of higher tonnage trucks, the introduction of new and improved higher tonnage models by original equipment manufacturers (OEMs) on a regular basis, and the constraints of driver shortage in the country. Furthermore, the improving road infrastructure with better and wider roads also eases the adoption of heavier and larger trucks.

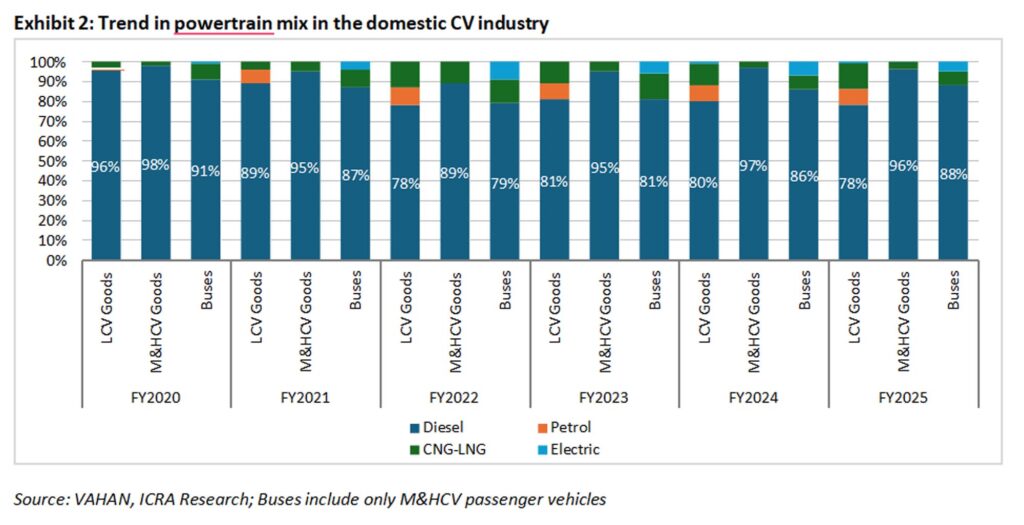

- Rise of alternative powertrains: Globally, the CV industry is expected to be one of the last ones to transit to electrification, given the range anxiety, extreme operating conditions and higher torque requirements, especially in the M&HCV segment. The domestic CV industry is no exception, although alternative powertrain penetration is gradually picking up, especially in segments like buses and LCVs. At present, conventional fuels (diesel and petrol) continue to dominate industry, with a penetration of around 87% in FY2025. However, there has been a gradual increase in the penetration of alternative fuels such as compressed natural gas (CNG) and liquified natural gas (LNG) in recent years, given the cost advantage over conventional fuels. The bus segment saw 5% electrification in FY2025. The increased traction for e-buses is not merely a function of the subsidies, but also favourable economics in terms of the total cost of ownership (TCO). Although operating costs get pushed upwards by the battery replacement costs and the requirement for on-site support for e-buses, overall, they remain favourable due to lower running costs, and thus, lower TCO even in absence of subsidiaries. Hence, ICRA estimates e-buses could offer 15-25% potential savings in terms of TCO. The rollout of the PM Electric Drive Revolution in Innovative Vehicle Enhancement Scheme (PM E- Drive) for e-trucks with effect from July 10, 2025, is also expected to support the pace of electrification in the trucks segment, which has so far seen limited adoption. ICRA expects electric penetration in the bus segment to reach around 30% by FY2030, and between 12-16% for the LCV segment. More recently, the OEMs are also working on hydrogen fuel cell and hydrogen internal combustion engine technologies; the acceptance of the same will depend on how much favourable the economics work out to be.

- Focus on driving comfort and efficiency improvement through regulatory interventions: In the recent years, the Government of India (GoI) has been updating motor vehicle emission standards for new vehicles and introducing additional aspects with a focus on improving driver comfort and safety. Such regulatory interventions have led to a series of price hikes by the CV OEMs over the years – the latest change in emission norms (BS VI 2.0), which came into effect in April 2023 led to around 5% price increase for CVs. Mandatory installation of air-conditioned cabins for trucks from October 2025 (which is likely to increase vehicle prices by Rs. 20,000-30,000, or 1-2% of vehicle price) is one of the key upcoming regulatory interventions in the domestic CV industry. Such interventions by the GoI are likely to improve vehicular efficiency and promote adoption of alternative powertrains in the coming years.

- Increased competition from railways: The next trend that ICRA expects to play out over the long term is some shift of freight from road to alternate modes of transport, especially rail, accelerated to some extent by the dedicated freight corridors (DFCs). With the trains plying on the DFCs longer and faster than the existing freight trains, their efficiency is better than the existing rail network, enabling them to eat into the share of roadways. A major impact is expected to be on the tractor trailer segment, especially since the Western DFC is likely to attract significant container traffic. However, in other sectors and commodities, the impact is not expected to be very significant, given the limited area that the DFC caters to at present, and the first and last mile transport requirements, which would continue to require CVs. That said, investments for enhancing road infrastructure also continue, with a lot of focus on development of highways, economic corridors, expressways etc. to enhance the efficiency of the road infrastructure. These also augur well for increasing efficiencies of the trucks for long-haul applications, and accordingly, fleet operator viability.

The growth drivers for the domestic CV industry remain intact and would draw support from the GoI’s sustained push in infrastructure development (evidenced by around 10% increase in its capital expenditure target to Rs. 11.2 trillion in FY2026), a steady increase in mining and infrastructure activities and the improvement in roads/highway connectivity. While factors like rapid urbanisation, resulting in an increasing need for mass transit and end-to-end connectivity for metro routes, would augur well for the demand outlook for the buses segment, expanding network of highways and the growth in e-commerce would likely fuel demand for the trucks segment.