LCVs to drive mild recovery this fiscal; price hikes to continue as compliance costs soar

By Anuj Sethi, Senior Director, Crisil Ratings

India’s commercial vehicle (CV) sector is expected to see a mild recovery this fiscal, with domestic volume expected to grow in low single-digits after a contraction last fiscal.

While the sector is inching closer to its pre-pandemic peak of fiscal 2019, the recovery has lagged those of other automotive segments due to volatility in the freight market, subdued rural sentiment, moderation in road construction activity and rising competition in the small commercial vehicle (sub 1 tonne) category.

This fiscal, improving infrastructure execution, supported by large government capital expenditure (capex), deferred fleet replacement and better exports are likely to arrest demand sluggishness.

And even as rising regulatory costs pressure will keep capex elevated, steady operating margin, along with the sector’s financial resilience, will support the credit profiles of CV original equipment manufacturers (OEMs) in the road ahead.

What is Driving Revival

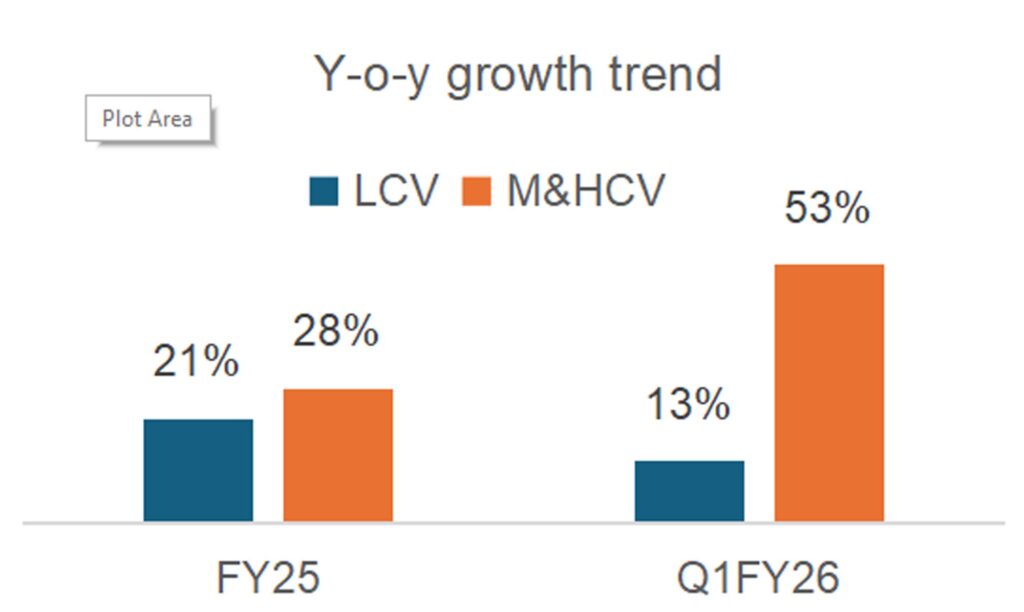

| Domestic volume growth expectation | ||

| Full year | Q1 (Apr-Jun) | |

| FY25 | -1.2% | 3.5% |

| FY26 | 2-4% | -0.6% |

After a degrowth in volume last fiscal, the sector’s turnaround this fiscal is being anchored by a sharp revival in infrastructure-led freight demand.

Central government capex reached 25% of budget allocation, providing a stable foundation for CV volume recovery.

In the first quarter of this fiscal, domestic sales volume declined marginally due to weak offtake of light commercial vehicles (LCVs).

Beginning the second quarter, however, the volume should pick up due to higher infrastructure execution, festive stocking, and improvement in rural liquidity. Easing inflation and interest rates will also help unlock deferred replacement demand.

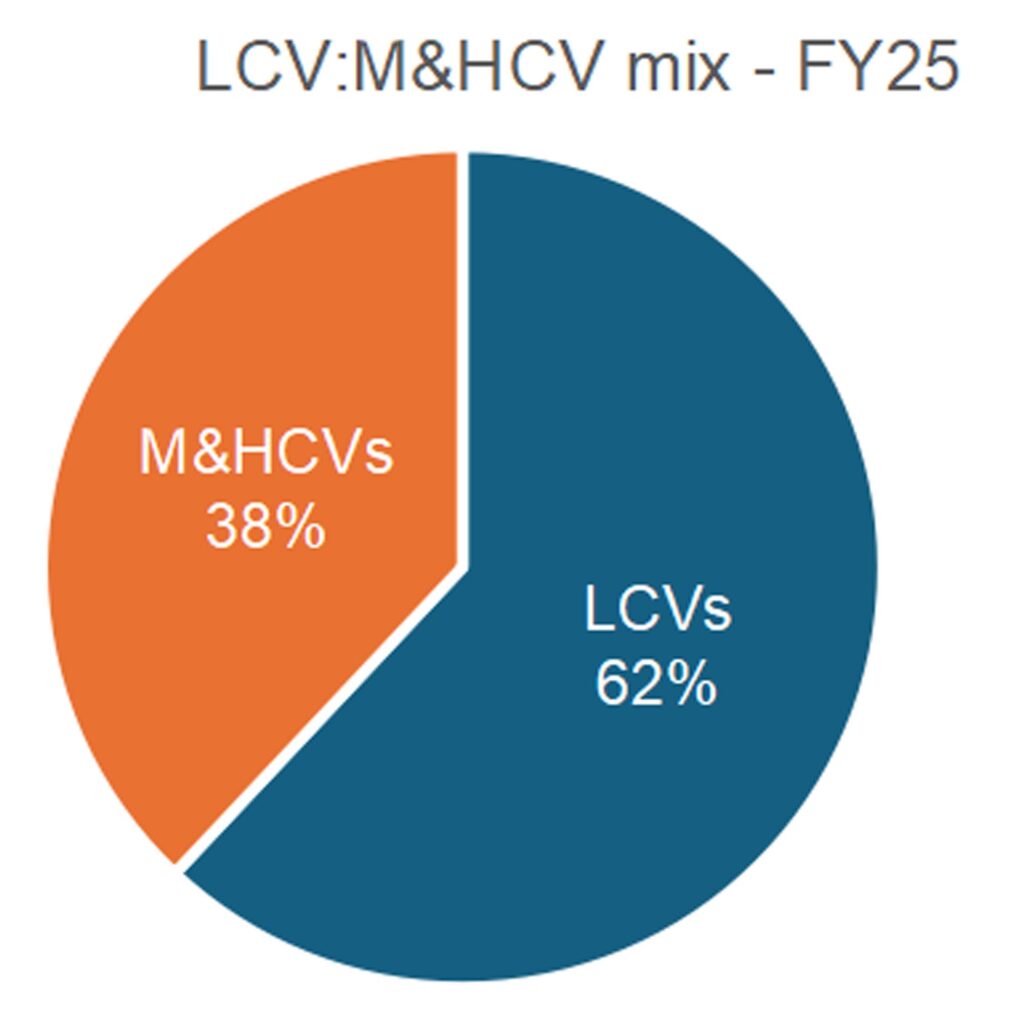

LCVs Leading the Upturn, MHCVs Riding the Infra Wave

LCV operators are shifting from sub-1/2 tonnes, which is facing strong competition from electric three-wheelers, to the 2-3.5 tonnes range for better load economics.

Sale volume of medium and heavy commercial vehicles (M&HCVs) is likely to grow 1-3% this fiscal, driven by pick-up in infrastructure execution, especially in the roads, metro rail, and industrial sectors.

Within M&HCVs, the high-tonnage 35-49 tonnes category continues to gain share, driven by freight efficiency, stricter axle norms, and longer-haul demand consolidation.

Electric Buses powering ahead on Policy Push, Low Base

Electric buses are gaining traction, though these are still a small slice (~3,200 units) of the total volume.

The Rs 57,613 crore PM-eBus Sewa scheme is driving demand aggregation by state transport undertakings. The scheme is expected to create long-term structural demand in the electric mobility ecosystem, prompting OEMs to invest in modular EV platforms and charging partnerships.

Exports Remain a Bright Spot

The OEMs reported healthy shipments to key markets in Africa, the Middle East, and Latin America. Demand in these regions is supported by infrastructure investments, fleet upgrades, and replacement cycles. Also, some of these nations have emerged from strained financial positions, which had impacted exports earlier.

With players strategically expanding into the Association of Southeast Asian Nations and East African corridors, the export volumes are expected to grow, providing an important hedge against domestic cyclicality, even as geopolitical risks and tariff uncertainties in certain trade zones prevail.

Profitability, Financial Risk Profile resilient despite Capex and Regulatory Requirements

| Sectoral forecast | ||

| FY25E | FY26P | |

| Ebitda margin (%) | 11.6% | 11-12% |

| Capex/Ebitda (x) | 0.3 | ~0.3 |

| Debt/Ebitda (x) | 1.0 | <1.0 |

| Interest coverage (x) | 14.1 | ~15.0 |

| Capex increase (%) | 14.0% | 12-15% |

The operating margin of players in the segment is likely to remain steady at 11-12% this fiscal, in line with last fiscal’s decadal high, driven by stable steel prices and calibrated pricing actions.

This fiscal will mark a regulatory pivot with mandatory air-conditioned cabins for trucks effective October 2025. This is expected to push up M&HCV prices by at least Rs 30,000 per unit. The OEMs already raised prices by 2-3% in January 2025 to absorb part of the compliance cost.

Capex is expected to rise 12-15% this fiscal, with leading OEMs planning ~Rs 4,500 crore investments for regulatory upgrades, safety compliance, and EV platforms.

Despite the investment uptick, debt levels should remain stable because of strong cash flows, stable profitability, and lean working capital. This will ensure financial risk profiles remain healthy.

From Compliance to Competitiveness

Over the past couple of years, CV technology has evolved significantly, riding on introduction of BS-VI norms, OBD-II upgrades, digital telematics, modular platforms and fuel-efficient drivetrains.

Fleet owners are increasingly adopting digital fleet management, preventive diagnostics, and EV optimisation. These shifts have collectively improved uptime, reduced maintenance, and boosted fleet utilisation and overall cost economics for fleet operators, thereby enhancing the competitiveness of organised transporters.

Key Watchpoints Ahead

While this fiscal notches a recovery phase for the CV sector, the pace remains measured.

The extent of infrastructure project execution, rural sentiments post-monsoon, interest rate trajectory and inflationary trends will be monitorable.

Regulatory cost absorption and its impact on demand will also bear watching.

Though domestic volumes this fiscal may not reclaim the all-time high sale volumes seen in fiscal 2019, the sector is clearly realigning for longer term strength with sharper focus on profitability and platform evolution.